Section 147A Reassessment Notices: What Taxpayers Should Know After Supreme Court’s Remand in JAO vs FAO Cases

SEO Title: Section 147A Reassessment Notices: Supreme Court Remands JAO vs FAO Cases

URL Slug: section-147a-reassessment-notices-supreme-court-remand

Meta Description: Section 147A reassessment notices face fresh High Court scrutiny after Supreme Court remands JAO vs FAO cases post Finance Act 2026 amendment.

Introduction

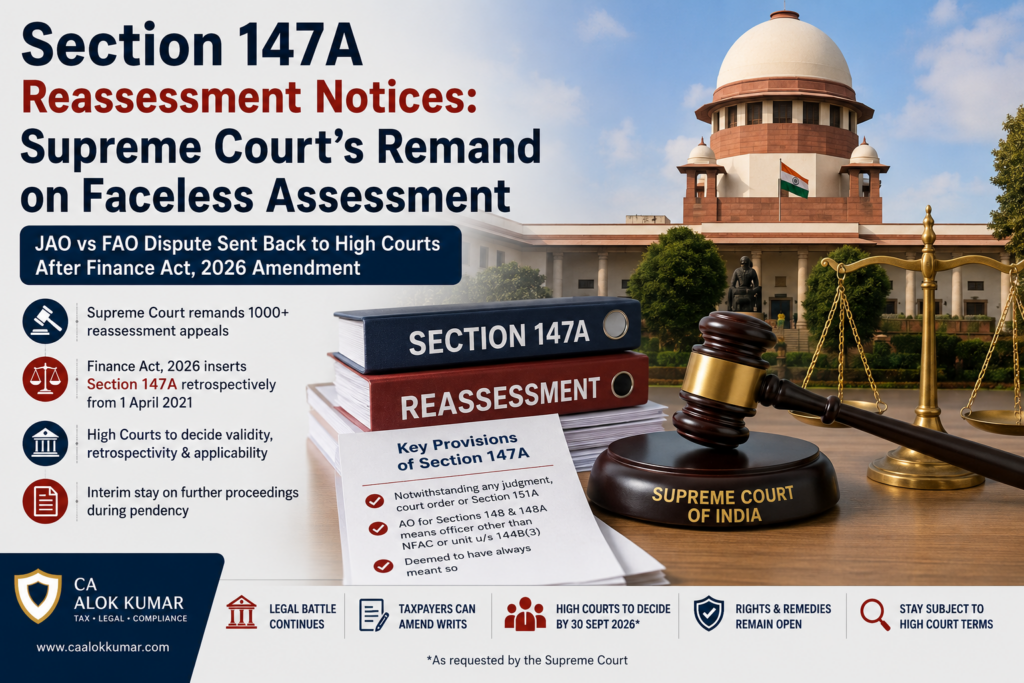

Section 147A reassessment notices have become one of the most important reassessment litigation issues under the Income-tax Act, 1961. The controversy relates to whether reassessment notices under Section 148 and orders under Section 148A should be issued by the Jurisdictional Assessing Officer, commonly referred to as JAO, or through the faceless mechanism.

The Supreme Court, in Income Tax Officer, Ward 2(1), Chandigarh & Ors. v. Tej Partap Singh, has not finally decided this controversy. Instead, after the insertion of Section 147A by the Finance Act, 2026, the Supreme Court has remitted the matter to the respective High Courts for fresh adjudication.

For a detailed professional note on this issue, readers may also refer to this published analysis on Section 147A reassessment notices by CA Alok Kumar.

Background: Why JAO vs FAO Became a Major Reassessment Dispute

After the Finance Act, 2021, the reassessment framework under Sections 147 to 151 was substantially changed. Section 148A introduced a pre-notice procedure before issuing a notice under Section 148. In many cases, the Assessing Officer is required to provide an opportunity to the assessee, consider the reply, and pass an order before issuing the reassessment notice.

Thereafter, the Central Government notified the e-Assessment of Income Escaping Assessment Scheme, 2022 through CBDT Notification No. 18/2022 dated 29 March 2022 under Section 151A. The scheme provided for a faceless mechanism and automated allocation in reassessment proceedings.

This created a legal dispute. Taxpayers argued that reassessment notices and Section 148A orders should have been issued through the faceless mechanism and not directly by the Jurisdictional Assessing Officer. Several High Courts accepted this argument, while some other High Courts took a different view.

As a result, the JAO vs FAO reassessment issue reached the Supreme Court in a large batch of matters.

What Finance Act, 2026 Changed Through Section 147A

The Finance Act, 2026 inserted Section 147A into the Income-tax Act, 1961 with retrospective effect from 1 April 2021.

Broadly, Section 147A states that notwithstanding any judgment, court order, Section 151A, or any scheme framed under Section 151A, the Assessing Officer for the purposes of Sections 148 and 148A shall mean, and shall always be deemed to have meant, an Assessing Officer other than the National Faceless Assessment Centre or any assessment unit referred to in Section 144B(3).

In simple terms, the amendment attempts to retrospectively clarify that the Jurisdictional Assessing Officer was competent to issue notices and pass orders under Sections 148 and 148A, despite the faceless reassessment scheme.

This amendment has changed the foundation of several High Court judgments where notices were quashed mainly on the ground that they were issued by JAOs and not through the faceless mechanism.

What the Supreme Court Decided in Tej Partap Singh

In ITO v. Tej Partap Singh, the Supreme Court observed that several High Court decisions had quashed reassessment notices because they were issued by the JAO instead of through the faceless system. Since Section 147A was later inserted retrospectively, the Court held that the matters required fresh consideration by the High Courts.

Accordingly, the Supreme Court set aside the impugned High Court judgments on this limited ground and remitted the matters to the respective High Courts.

The Court also permitted assessees to amend their writ petitions to challenge Section 147A or any connected provision. The Revenue was also given liberty to file its submissions and affidavits.

Most importantly, the Supreme Court did not express any final opinion on the validity, scope, effect, retrospectivity or applicability of Section 147A. All these issues were left open for the High Courts.

Does This Mean All JAO-Issued Notices Are Now Valid?

No. This is the most important practical point.

The Supreme Court has not upheld every notice issued by a Jurisdictional Assessing Officer. It has also not finally rejected the taxpayer’s challenge. The Court has only recognised that the law has changed due to Section 147A and that High Courts must now examine the matter afresh.

Therefore, taxpayers should not treat the Supreme Court order as an automatic validation of all reassessment notices. At the same time, taxpayers should also not assume that earlier favourable High Court decisions will automatically continue to protect them without further legal examination.

Interim Stay and High Court Timeline

The Supreme Court directed that further assessment or reassessment proceedings pursuant to the impugned notices shall remain stayed during the pendency of the writ petitions before the High Courts, subject to terms and conditions imposed by the concerned High Courts.

The High Courts have also been requested to decide the remanded matters preferably by 30 September 2026.

This means affected taxpayers should closely monitor their pending writ petitions, reassessment records and High Court directions.

What Taxpayers Should Check After Section 147A

After the insertion of Section 147A, the dispute is no longer limited to the technical issue of whether the notice was issued by the JAO or through the faceless system.

Taxpayers should now examine the reassessment record on multiple grounds, including:

- Whether there was valid information suggesting escapement of income

- Whether the Section 148A(b) notice supplied proper material

- Whether the assessee’s reply was properly considered

- Whether the Section 148A(d) order shows application of mind

- Whether sanction under Section 151 was validly obtained

- Whether the notice was within limitation under Section 149

- Whether the case is based on borrowed satisfaction

- Whether the issue is merely a change of opinion

- Whether the retrospective amendment can constitutionally cure the defect

Where the reassessment is being conducted through the online mechanism or faceless framework, proper faceless assessment representation becomes important because every reply, document and submission should be carefully drafted and uploaded within time.

Demand Notice Risk After Reassessment

A reassessment notice may ultimately result in an addition and tax demand. Therefore, taxpayers should not respond casually or only on the basis of portal-generated information.

If a demand has already been raised, or if a reassessment order results in a demand, taxpayers should take proper assistance for income tax demand notice response before accepting, disputing or paying the demand.

A correct demand response may require reconciliation of the assessment order, Form 26AS, AIS/TIS, challans, TDS credit, interest calculation and earlier submissions made during the reassessment proceedings.

Importance of Correct ITR and Disclosure Review

Many reassessment proceedings arise due to mismatch in income reporting, incorrect return selection, non-disclosure of high-value transactions, wrong claim of deductions, incorrect capital gains reporting or mismatch in AIS/TIS.

In such cases, taxpayers may need to review whether the original return was correctly filed. Where the nature of income or disclosure requires specialised review, services such as ITR-B filing may become relevant depending on the facts of the case.

Taxpayers should also preserve the complete return filing record, computation, Form 16, Form 26AS, AIS, TIS, bank statements and supporting documents.

Can ITR-U Be Filed After a Reassessment Notice?

An updated return under Section 139(8A) can be useful in some situations where the law permits correction of income. However, it is not available in every case, especially where statutory restrictions apply or proceedings have already reached a particular stage.

Before considering ITR-U updated return filing, taxpayers should carefully verify the assessment year, notice status, limitation period and restrictions under Section 139(8A).

A wrong or hurried ITR-U strategy may create additional complications in reassessment proceedings.

NRI, Foreign Remittance and Reassessment Issues

Reassessment notices may also arise in cases involving NRI income, sale of property by non-residents, remittance from NRO to NRE accounts, foreign assets, foreign bank accounts, overseas income or mismatch in foreign remittance reporting.

In such cases, the taxpayer may need to reconcile bank credits, capital gains, TDS, Form 26AS, AIS and remittance documents. Where funds are proposed to be remitted outside India, taxpayers may also require professional support for Form 145-146 CA certificate for foreign remittance.

Tax Exposure and Relief Calculation

In reassessment matters, taxpayers should estimate the possible tax, interest and demand exposure before finalising litigation or settlement strategy.

A preliminary calculation using an income tax relief calculator may help in understanding the broad impact. However, final tax liability must always be reviewed with reference to the assessment order, applicable provisions, interest computation and facts of the case.

Key Takeaway

The Supreme Court’s order in Tej Partap Singh is not a final approval of all reassessment notices issued by JAOs. It is also not a final victory for taxpayers. The Court has remitted the matters to the High Courts because Section 147A has changed the statutory position retrospectively.

The real litigation will now focus on whether Section 147A is valid, whether it can operate retrospectively, whether it cures the alleged defect, and whether each reassessment notice is otherwise valid on facts and law.

Taxpayers dealing with Section 147A reassessment notices should review the complete record carefully and avoid mechanical replies. The defence should cover jurisdiction, limitation, sanction, natural justice, material relied upon, application of mind and factual correctness.

FAQs on Section 147A Reassessment Notices

1. What is Section 147A?

Section 147A is a provision inserted by the Finance Act, 2026 with retrospective effect from 1 April 2021. It clarifies the meaning of Assessing Officer for the purposes of Sections 148 and 148A.

2. What is the JAO vs FAO reassessment dispute?

The dispute is whether reassessment notices under Section 148 and orders under Section 148A should have been issued by the Jurisdictional Assessing Officer or through the faceless reassessment mechanism.

3. Did the Supreme Court decide the validity of Section 147A?

No. The Supreme Court did not decide the validity, scope, effect, retrospectivity or applicability of Section 147A. These issues have been left open for the High Courts.

4. Are all JAO-issued notices valid after Section 147A?

Not automatically. Taxpayers can still challenge notices on grounds such as limitation, sanction, lack of material, non-application of mind, violation of natural justice and constitutional validity of retrospective amendment.

5. What should taxpayers do after receiving a Section 148 notice?

Taxpayers should collect the Section 148A notice, reply filed, Section 148A(d) order, Section 148 notice, approval under Section 151, assessment records, AIS/TIS, Form 26AS and all supporting documents before filing any reply.

6. Is professional review necessary in reassessment cases?

Yes. Reassessment cases involve limitation, jurisdiction, facts, documents, tax computation and legal strategy. A casual response may weaken the taxpayer’s case.

Suggested Tags

Section 147A, Reassessment Notice, Section 148 Notice, Section 148A Order, JAO vs FAO, Faceless Reassessment, Income Tax Notice, Finance Act 2026, Section 151A, Tej Partap Singh Supreme Court

Suggested Image Alt Text

Section 147A reassessment notices after Supreme Court remand in JAO vs FAO faceless assessment cases.

Suggested Social Sharing Line

Supreme Court has remanded JAO vs FAO reassessment cases after the retrospective insertion of Section 147A. Taxpayers should now review jurisdiction, limitation, sanction, natural justice and factual grounds carefully.

You may publish this as a separate TaxParley article without creating duplicate-content risk, as the structure, wording and flow are substantially different from the caalokkumar.com version.