Section 54 Exemption for Multiple Houses: ITAT Bangalore Clarifies Asset-wise Capital Gains Relief

The ITAT Bangalore ruling in Pavan Kumar Agarwal v. DCIT, Central Circle-2(3), Bengaluru is an important decision for taxpayers who sell multiple residential houses in one financial year and reinvest the capital gains in residential property.

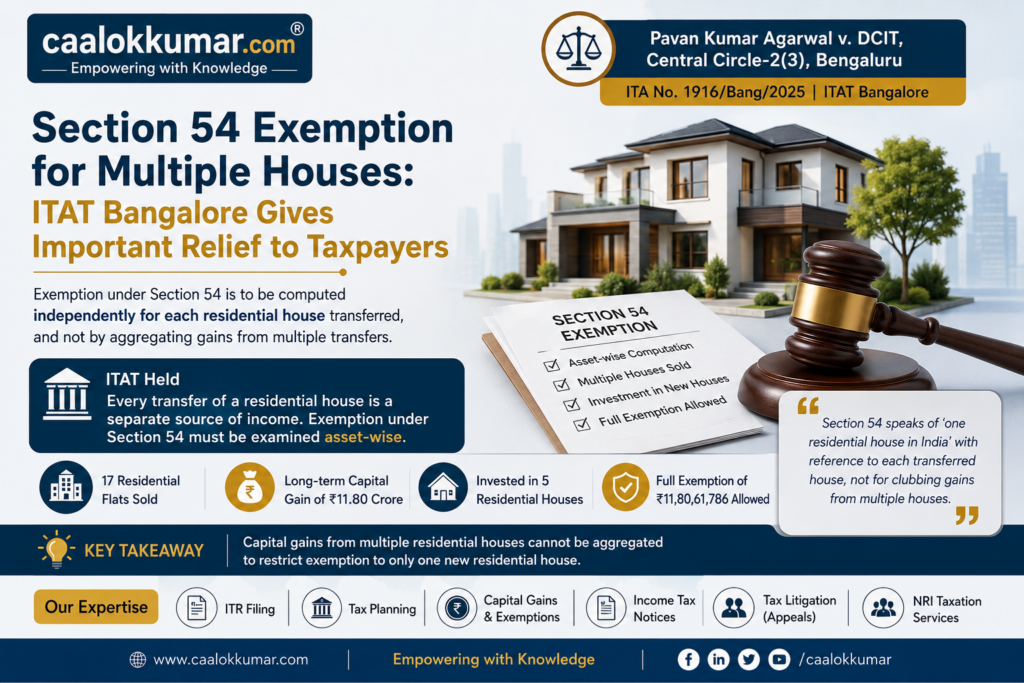

The key question before the Tribunal was whether exemption under Section 54 should be computed separately for each residential house transferred, or whether the capital gains from all residential houses sold during the year should be clubbed together and restricted to investment in only one residential house.

The Tribunal held in favour of the assessee.

In this case, the assessee had received several flats under Joint Development Agreements. During AY 2020-21, he sold 17 residential flats and earned long-term capital gains of ₹11.80 crore. The gains were reinvested in construction of one residential house and purchase of four other residential houses. The assessee claimed exemption under Section 54 for the entire amount.

The Assessing Officer relied on the amendment in Section 54, where the expression “a residential house” was replaced with “one residential house in India”, and restricted the exemption to the cost of only one house. This resulted in disallowance of ₹5.88 crore. The CIT(A) confirmed the addition.

The ITAT held that capital gains under Sections 45 and 48 must be computed separately for each capital asset transferred. Every residential house sold is a separate capital asset and every transfer constitutes a separate source of capital gain. Aggregation takes place only after computation; it does not erase the identity of each asset.

Therefore, exemption under Section 54 must also be examined asset-wise.

The Tribunal clarified that the 2014 amendment restricting investment to “one residential house in India” applies with reference to the capital gain arising from each transferred residential house. It does not mean that all gains from multiple residential houses sold during the year must be clubbed together and exemption restricted to only one new house.

This ruling is particularly useful for property sellers, landowners receiving flats under Joint Development Agreements, families selling inherited residential units, and taxpayers facing capital gains scrutiny.

Taxpayers can read the detailed analysis here: Section 54 exemption for multiple houses.

For practical compliance, taxpayers should carefully prepare the capital gain computation, reinvestment mapping and Schedule CG disclosure. A preliminary estimate may be made using a capital gain tax calculator, but the final exemption claim should be aligned with supporting documents and the correct ITR form.

Where a taxpayer is filing ITR-2 or ITR-3 with property capital gains, professional ITR filing with capital gains disclosure can help avoid mismatch in AIS, TIS, Form 26AS, sale consideration, stamp duty value and exemption reporting.

If exemption under Section 54 is disallowed during assessment, the taxpayer should examine whether an appeal, rectification, demand stay or detailed response is required. Relevant support may be taken for income tax demand notice response and tax litigation and ITAT appeal support.

In property transactions, TDS compliance is equally important. Buyers and sellers should also review TDS on sale of property, especially where Form 26QB, NRI seller issues or lower TDS certificate planning is involved.

The detailed article is available here: Section 54 exemption for multiple houses.

Key Takeaway:

Section 54 exemption should be examined independently for each residential house transferred. Capital gains from multiple residential houses cannot be automatically clubbed merely to restrict exemption to investment in one new house.