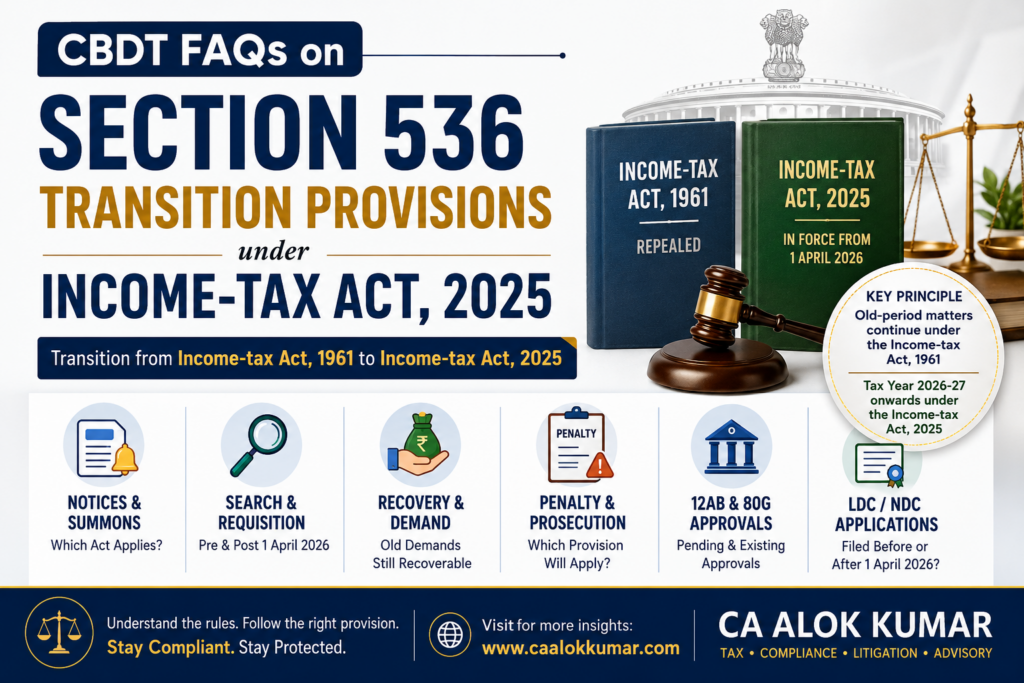

The Central Board of Direct Taxes has issued important clarificatory FAQs on the transition provisions under Section 536 of the Income-tax Act, 2025, dealing with the repeal of the Income-tax Act, 1961 and the continuation of pending or old-period proceedings.

The FAQs are important for taxpayers, Chartered Accountants, tax professionals, companies, trusts, NRIs and businesses because the Income-tax Act, 2025 has come into force from 1 April 2026, but many assessments, notices, searches, recovery proceedings, penalty matters and applications may still relate to earlier years.

In simple words, the key question is:

Which law will apply after 1 April 2026 — the Income-tax Act, 1961 or the Income-tax Act, 2025?

CBDT has now clarified this issue through 23 FAQs covering summons, notices, search proceedings, jurisdiction transfer, provisional attachment, recovery, penalties, prosecution, charitable registrations, 12AB/80G approvals and lower deduction or no deduction certificate applications.